Learn about IRS Form 1099-B, its role in reporting precious metals transactions, including gold, silver, platinum, and palladium, and its tax implications.

Understanding the Role of Form 1099-B in Precious Metals Transactions

Form 1099-B is a vital IRS tax form used to report sales of various assets, including precious metals like gold, silver, platinum, and palladium. This form ensures that taxpayers accurately report any gains or losses made from the sale of precious metals, helping maintain tax compliance.

If you're involved in buying or selling precious metals, understanding the requirements for Form 1099-B is crucial to avoid tax issues and to stay compliant with IRS tax laws.

Key IRS Authority for Precious Metals Reporting

The IRS requires precious metals dealers to file Form 1099-B for specific transactions, as outlined in Revenue Procedure 92-103. This procedure defines the reporting requirements, focusing primarily on metals traded on regulated commodities exchanges.

To determine which metals are reportable, the IRS defers to the Commodity Futures Trading Commission (CFTC), which sets the purity, type, and quantity thresholds that make a metal eligible for reporting under Form 1099-B.

Precious Metals Dealers, 1099-B Filing, and Reporting Standards

Precious metals dealers and brokers may be required to file IRS Form 1099-B when customers sell certain bullion products back to a dealer in quantities that meet established reporting thresholds. These rules were originally defined under IRS Revenue Procedure 92-103, which outlines when brokers must report the sale of metals that resemble standardized exchange-traded bullion contracts.

In practice, reporting requirements depend on several factors, including the type of metal, product form, purity, and quantity involved, rather than simply the dollar value of a transaction. The thresholds historically mirrored the deliverable contract sizes used in professional bullion and futures trading markets, which is why most reporting rules apply only to very large wholesale-style quantities.

While earlier guidance included a broader list of reportable products, industry interpretation has evolved over time. Dealers now commonly follow updated compliance practices that better reflect how large bullion contracts are traded in modern markets.

The examples below illustrate the typical bullion products and quantities that may trigger Form 1099-B reporting when sold to a dealer.

Gold Reporting Thresholds

Historically, certain gold bullion coins and bars triggered Form 1099-B reporting when sold in bulk quantities. Traditional reporting guidelines included:

-

25 or more one-ounce Gold Maple Leaf coins

-

25 or more one-ounce Gold Krugerrand coins

-

25 or more one-ounce Mexican Gold Libertads (Onzas)

-

Gold bars totaling one kilogram (32.15 troy ounces) or more

-

Gold bars with a minimum fineness of .995

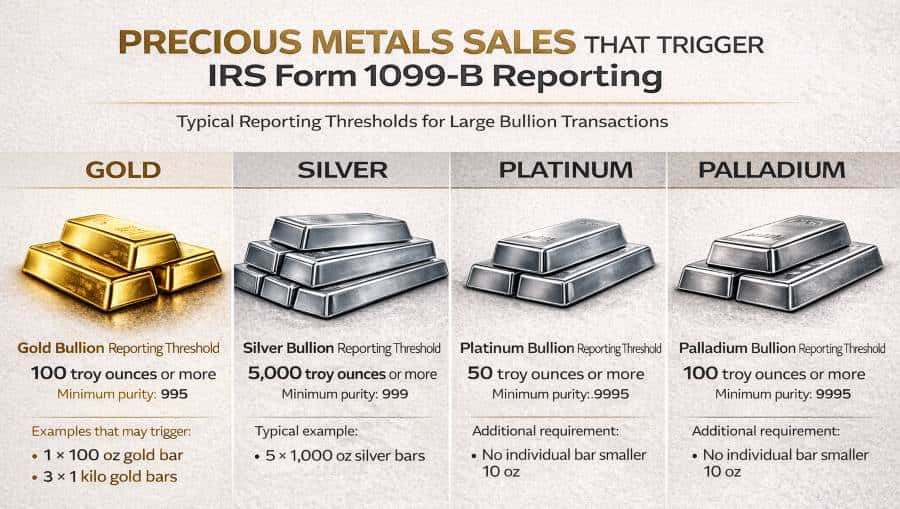

Industry interpretation has since shifted for large gold bars. Current guidance widely followed by bullion dealers indicates that reporting typically applies when a customer sells:

-

One 100-troy-ounce gold bar, or

-

Three or more one-kilogram gold bars (approximately 96.45 troy ounces total)

-

Minimum purity: .995

These thresholds reflect standard bullion contract sizes used in professional trading markets.

Silver Reporting Thresholds

Silver reporting guidelines have also evolved over time.

Historically, reporting applied when investors sold:

-

Silver bars or rounds totaling 1,000 troy ounces

-

90% U.S. silver coins exceeding $1,000 face value

Current industry guidance indicates that 90% U.S. silver coins generally no longer require Form 1099-B reporting.

Instead, reporting typically applies only to very large wholesale transactions involving:

-

Five or more 1,000-troy-ounce silver bars

-

Total quantity of 5,000 troy ounces

-

Minimum purity: .999

Because most investors buy and sell silver in much smaller quantities, these thresholds are rarely reached in typical retail bullion transactions.

Platinum Reporting Thresholds

Platinum reporting rules have also been revised compared with earlier guidance.

Historically, reporting applied when 25 troy ounces or more of platinum bullion were sold.

Current industry interpretation generally indicates that reporting applies when:

-

50 troy ounces or more of platinum are sold

-

The bullion consists of bars weighing 10 troy ounces or more

-

Minimum purity: .9995

Because most platinum bullion bars sold to investors weigh 1 troy ounce, many investors will never encounter this reporting requirement.

Palladium Reporting Thresholds

Palladium reporting thresholds have remained relatively consistent over time.

Historically and under current interpretation, reporting typically applies when:

-

100 troy ounces or more of palladium bullion are sold

-

The transaction includes palladium bars weighing 10 ounces or more

-

Minimum purity: .9995

Since most palladium bullion products available to investors are 1-ounce bars, reaching this threshold is uncommon for retail transactions.

Why Most Bullion Sales Are Not Reportable

Although Form 1099-B reporting rules exist for certain precious metals transactions, they primarily apply to large institutional-scale bullion sales.

Because the thresholds involve substantial quantities—such as multiple kilogram gold bars or several thousand ounces of silver—most investors buying or selling coins or smaller bullion bars will not reach the levels required to trigger reporting.

Precious metals dealers must still follow IRS compliance rules and may apply reporting standards conservatively depending on their interpretation of regulatory guidance. However, in everyday retail bullion transactions, Form 1099-B reporting is rarely triggered.

What Types of Precious Metals Are Not Reportable?

The IRS does not require reporting on all precious metals. Specifically, Form 1099-B does not apply to:

-

Fractional bullion: Metals that do not meet the exchange deliverable thresholds.

-

Coins: Most bullion coins (like American Gold Eagles and Silver Eagles) are not reportable, as they don’t meet CFTC deliverable standards.

-

Numismatic coins: Rare or collectible coins are typically not reportable, unless they are specifically required under other IRS rules.

-

Jewelry or scrap metals: These types of transactions do not trigger the need for a 1099-B filing.

The key factor is that IRS reporting requirements apply primarily to metals that meet the CFTC’s exchange deliverable standards for futures trading, which is why common bullion coins and smaller bars are typically not covered by this form.

Do Gold Purchases Have to Be Reported to the IRS?

Many investors entering the precious metals market wonder whether buying gold or silver automatically triggers IRS reporting. In most situations, simply purchasing precious metals does not require reporting to the IRS.

The IRS does not require individuals to disclose ownership of physical bullion such as gold, silver, platinum, or palladium. Investors can legally buy coins or bullion bars from dealers without filing a report with the government simply because the purchase occurred.

Confusion usually arises because certain transaction structures, rather than the metal itself, can trigger reporting obligations for dealers. For example:

-

Cash payments exceeding $10,000 may require a dealer to submit IRS Form 8300.

-

Large bullion sales back to a dealer may trigger Form 1099-B reporting if the metal type and quantity meet specific thresholds.

In these cases, the reporting responsibility typically falls on the dealer or broker handling the transaction, not the individual purchasing the metal.

However, investors should remember that profits from selling precious metals may be subject to capital gains tax. When bullion is sold for more than its original purchase price, those gains generally must be reported on the investor’s tax return.

For most investors buying standard bullion coins or small bars, purchasing precious metals alone does not create a reporting requirement with the IRS.

When Is Form 1099-B Filed for Precious Metals?

Form 1099-B is filed when the sale of precious metals meets the following criteria:

-

The transaction involves metals that meet CFTC deliverable standards (as outlined above).

-

The metal sold meets the IRS reportable thresholds for size, weight, and purity.

If a precious metals dealer facilitates a sale that meets these criteria, they are required to file Form 1099-B with the IRS to report the transaction. However, it’s important to note that the dealer is only responsible for reporting the sale price of the merchandise to the IRS, not the buyer's purchase basis. Buyers must self-report their basis (the original purchase price) when filing their taxes. Dealers do not provide the basis for the sale—only the details of the transaction itself.

What Should Investors Know About 1099-B Reporting?

Investors involved in larger precious metals transactions should understand how Form 1099-B fits into the IRS reporting process. Although dealers are responsible for filing Form 1099-B, investors must accurately report their gains or losses on their tax returns based on the information provided by the dealer. This includes self-reporting the basis for the sale (the original purchase price) on your tax return.

If you’re involved in significant bullion transactions or cash-based purchases, it’s highly advisable to consult a tax professional to ensure you remain in compliance with IRS regulations and avoid complications during tax season.

Understanding Form 1099-B and Precious Metals Transactions

Although IRS reporting requirements exist for certain bullion transactions, they generally apply only to specific metals sold in large quantities that meet established reporting thresholds. Most investors buying or selling standard bullion coins or smaller bars will never encounter Form 1099-B reporting. Understanding how these rules work helps investors navigate precious metals markets with greater confidence while avoiding confusion about common myths surrounding gold and silver reporting.

Key Takeaways

-

Form 1099-B is used to report precious metals sales, including gold, silver, platinum, and palladium.

-

Dealers are required to file this form for transactions involving specific types of precious metals that meet CFTC exchange deliverable standards.

-

Form 1099-B helps ensure tax compliance by reporting the sale of the CFTC outlined items.

-

It’s essential for investors to understand their tax reporting obligations and consult a tax professional when needed.

Final Note

Please note that this article provides a general overview of Form 1099-B and its requirements for precious metals transactions. Tax laws and regulations can change, so for the most accurate and up-to-date information regarding your specific tax situation, we recommend consulting with a certified tax professional or accountant. You can also visit the official IRS website for further details on Form 1099-B.

FAQs

What is IRS Form 1099-B?

Form 1099-B is an IRS tax form used to report proceeds from the sale of certain assets, including qualifying precious metals transactions.

When is Form 1099-B required for precious metals?

A 1099-B is required when a precious metals sale meets IRS reportable thresholds based on CFTC deliverable standards for size, weight, and purity.

Which precious metals are reportable on Form 1099-B?

Reportable items include qualifying gold, silver, platinum, and palladium bars, as well as certain gold coins sold in bulk quantities that meet exchange standards.

Are gold and silver coins always reportable?

No. Most bullion coins, including American Gold Eagles and Silver Eagles, are not reportable because they do not meet CFTC deliverable standards.

What gold bars must be reported on Form 1099-B?

Gold bars are reportable if they weigh 100 troy ounces or meet the industry-recognized equivalent of three 1-kilo bars with .995 minimum fineness.

Who is responsible for filing Form 1099-B?

The precious metals dealer files Form 1099-B for qualifying transactions, reporting the sale proceeds to the IRS.

Does the dealer report my purchase basis on Form 1099-B?

No. Dealers report only the sale price of the metals; investors must self-report their cost basis when filing their tax return.

What precious metals transactions are not reportable?

Fractional bullion, most bullion coins, numismatic coins, and jewelry or scrap metals are generally not subject to Form 1099-B reporting.

Should I consult a tax professional about Form 1099-B?

Yes. Because tax situations vary and regulations can change, consulting a qualified tax professional helps ensure accurate reporting and compliance.

Related reading you may find interesting:

Buying Gold Through Your Financial Advisor: What Investors Should Know