IRS Reporting Rules for Gold and Silver Investors Explained

Understanding IRS Precious Metals Reporting Rules in 2026

Physical precious metals continue to attract investors seeking stability in an uncertain financial environment. As the gold spot price and silver spot price fluctuate alongside inflation concerns, geopolitical tensions, and shifting monetary policy, more individuals are turning to bullion as a way to diversify portfolios and protect purchasing power.

At the same time, rumors about government reporting requirements for gold and silver frequently circulate online. In recent months, claims have spread suggesting that new IRS rules dramatically lowered reporting thresholds or require investors to disclose their precious metals holdings.

In reality, most of these claims stem from misunderstandings of long-standing reporting rules. While certain large transactions involving bullion may trigger reporting obligations for dealers, simply owning gold or silver does not require disclosure to the IRS. Understanding how these rules actually work can help investors navigate the precious metals market with confidence.

Why Precious Metals Transactions Are Reported

Federal reporting requirements related to precious metals were introduced decades ago as part of broader financial transparency laws. These regulations were designed to help authorities monitor potential money laundering and tax evasion in large financial transactions.

Importantly, these rules apply primarily to dealers and businesses, not individual investors. Reporting requirements are triggered by the structure of a transaction, including the payment method or the type of product being sold, rather than the simple fact that someone owns precious metals.

For investors who follow movements in the gold price, the silver market, or broader commodity trends, these reporting rules typically affect only a small subset of transactions.

The $10,000 Cash Rule and Form 8300

One of the most widely discussed reporting rules involves IRS Form 8300, which applies to large cash payments received by businesses.

When a precious metals dealer receives more than $10,000 in cash, the dealer must file Form 8300 with the IRS. This requirement applies if the payment occurs in a single transaction or in related transactions within a short time period.

What the IRS Considers “Cash”

For reporting purposes, the IRS includes several instruments under the definition of cash:

-

U.S. or foreign currency

-

cashier’s checks

-

money orders

-

bank drafts

-

traveler’s checks

If several of these instruments are used together and their combined value exceeds $10,000, the transaction becomes reportable.

Payment Methods That Do Not Trigger Form 8300

Many common payment methods used when purchasing bullion do not qualify as cash under this rule. These include:

-

bank wire transfers

-

personal checks

-

credit cards or debit cards

-

ACH transfers

-

electronic payment systems

For example, purchasing $40,000 worth of gold bullion by bank wire would not trigger Form 8300 reporting.

This distinction often surprises investors entering the precious metals market for the first time.

Do You Have to Report Gold Purchases to the IRS?

One of the most common questions new bullion investors ask is whether they must report gold or silver purchases to the IRS.

In most cases, the answer is no.

The IRS does not require investors to report simply buying or owning physical precious metals, including gold, silver, platinum, or palladium. Purchasing bullion coins or bars—whether online, from a dealer, or at a coin shop—does not create a reporting obligation for the buyer.

However, reporting rules can apply in certain situations involving the structure of the transaction, rather than the metal itself.

For example:

-

Cash payments exceeding $10,000 may require the dealer to file IRS Form 8300.

-

Certain large bullion sales back to a dealer may trigger Form 1099-B reporting if the transaction meets specific quantity and purity thresholds.

Importantly, these forms are generally filed by the dealer or business involved in the transaction, not by the investor simply because they purchased bullion.

Investors are only responsible for reporting taxable gains if they sell precious metals for a profit. Like other investment assets, precious metals may be subject to capital gains tax when sold for more than the original purchase price.

For most buyers purchasing coins or small bullion bars, no IRS reporting is required at the time of purchase.

When Precious Metals Sales Trigger Form 1099-B

A different IRS reporting rule may apply when investors sell certain precious metals back to a dealer. In these situations, the dealer may be required to submit IRS Form 1099-B, which reports the transaction to the Internal Revenue Service.

This form is different from Form 8300, which applies to large cash payments when metals are purchased. Instead, Form 1099-B reporting applies when specific bullion products are sold to a dealer, and the requirement is based on the type of metal, product form, purity, and quantity sold, rather than simply the dollar value of the transaction.

Because these rules typically apply to large wholesale-style transactions, most retail bullion investors never encounter Form 1099-B reporting.

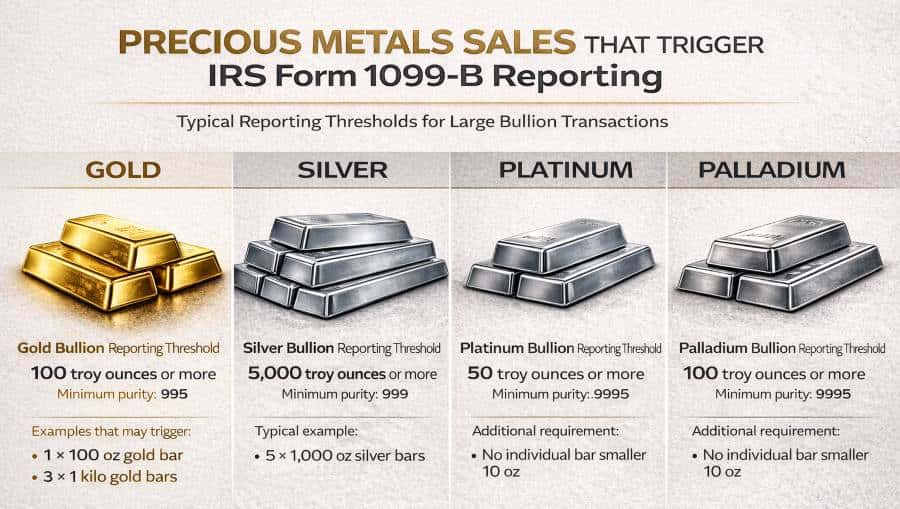

Gold 1099-B Reporting Thresholds

Historically, certain gold bullion products triggered reporting when sold in large quantities. Dealers traditionally reported sales involving:

-

25 or more one-ounce Gold Maple Leaf coins

-

25 or more one-ounce Gold Krugerrands

-

25 or more one-ounce Mexican Gold Libertads (Onzas)

-

Gold bars totaling one kilogram (32.15 troy ounces) or more

-

Gold bars with a minimum fineness of .995

Industry interpretation has evolved in recent years. While some dealers still follow these traditional guidelines for certain gold coins as a conservative compliance practice, consensus has shifted regarding large gold bars.

Current guidance widely followed by bullion dealers indicates that reporting typically applies when a customer sells:

-

One 100-troy-ounce gold bar, or

-

Three or more kilogram gold bars (about 96.45 troy ounces total)

These thresholds reflect the bulk contract sizes commonly used in the professional bullion market.

Silver 1099-B Reporting Thresholds

Silver reporting requirements have also changed over time.

Historically, reporting applied to transactions involving:

-

Silver bars or rounds totaling 1,000 troy ounces

-

90% U.S. silver coins exceeding $1,000 face value

Updated guidance now indicates that 90% U.S. silver coins no longer require 1099-B reporting.

Instead, reporting typically applies only to very large transactions totaling 5,000 troy ounces or more, usually consisting of five or more 1,000-ounce silver bars.

Because most investors buy and sell silver in much smaller quantities, this threshold is rarely encountered in retail bullion transactions.

Platinum 1099-B Reporting Thresholds

Platinum bullion reporting rules have also been revised.

Historically, reporting applied when investors sold 25 troy ounces or more of platinum bullion.

Current industry guidance generally indicates that reporting applies when:

-

50 troy ounces or more of platinum are sold

-

The bullion consists of bars weighing 10 ounces or more

-

The metal has a minimum fineness of .9995

Because most platinum bullion bars available to investors weigh 1 troy ounce, many investors will never encounter this reporting requirement.

Palladium 1099-B Reporting Thresholds

Palladium reporting thresholds have remained relatively consistent.

Historically, reporting applied when investors sold 100 troy ounces or more of palladium bullion.

Current interpretation maintains the 100-ounce reporting threshold, but it typically applies only when the transaction includes:

-

Palladium bars weighing 10 ounces or more

-

A minimum fineness of .9995

-

A total quantity of 100 ounces or greater

Since most palladium bullion bars sold to investors are 1-ounce bars, reaching this threshold is uncommon in typical retail transactions.

Why Most Bullion Investors Never Trigger Form 1099-B

Although IRS reporting rules exist for certain bullion transactions, they generally apply only to large institutional-scale quantities of metals.

Because the thresholds involve significant volumes—such as multiple kilogram gold bars or several thousand ounces of silver—most individual investors buying or selling coins and small bullion bars never reach the levels that require reporting.

Dealers still follow IRS compliance rules and may apply reporting standards conservatively depending on their interpretation of current guidance. However, for most retail bullion transactions, Form 1099-B reporting is rarely triggered.

Precious Metals Products Exempt From 1099-B Reporting

Many popular bullion products commonly purchased by investors are not included in traditional reporting lists.

Examples frequently cited within the industry include:

-

American Gold Eagle coins

-

American Silver Eagle coins

-

fractional gold bullion coins

-

various modern government-minted bullion coins

Because several of these bullion products were introduced after many reporting guidelines were originally drafted, they are not included in the historical list of reportable items.

Nevertheless, investors planning large transactions should always confirm reporting details with their dealer.

Capital Gains and Taxes on Precious Metals

It is important to distinguish between transaction reporting and tax obligations.

The IRS does not tax the act of buying or selling precious metals. Instead, taxes apply only to profits realized when metals are sold for more than their purchase price.

Precious metals are generally classified as collectibles for tax purposes, which means gains may be subject to a specific capital gains rate.

Understanding tax treatment is only part of the process. Investors should also maintain accurate records of their transactions.

Why Recordkeeping Matters

Maintaining accurate records helps investors calculate taxable gains if metals are sold. Important information to keep includes:

-

purchase dates

-

purchase price (cost basis)

-

product descriptions

-

sale prices

Accurate documentation ensures investors can properly report transactions if required.

Clearing Up the March 1 Precious Metals Reporting Rumor

Another rumor that gained traction online claims that a new IRS rule taking effect on March 1 requires Americans to report their gold and silver holdings, including where they are stored and how much is owned.

This claim is incorrect.

There is no federal rule requiring investors to disclose their precious metals ownership or register their bullion holdings.

The confusion appears to come from unrelated regulatory changes involving real estate transaction reporting rules that took effect March 1 for certain property purchases involving legal entities. These regulations fall under financial crime monitoring laws and do not apply to private precious metals ownership.

Where the $3,000 and $600 Reporting Rumors Came From

Additional misinformation has circulated suggesting that the IRS lowered precious metals reporting thresholds to $3,000 or even $600.

Neither number applies to bullion purchases or sales.

The $600 Rule Explained

The $600 figure comes from proposed reporting requirements related to Form 1099-K, which involves income received through certain third-party payment platforms and online marketplaces.

These rules relate to digital payment reporting and do not govern purchases of physical gold or silver from precious metals dealers.

The $3,000 Figure Explained

The $3,000 number originates from certain anti-money-laundering recordkeeping thresholds discussed in financial regulatory proposals affecting investment advisers and financial institutions.

These provisions involve internal compliance monitoring and do not establish a reporting threshold for gold or silver investors.

Because these regulatory changes appeared around the same time, many online discussions mistakenly linked them to precious metals purchases.

In reality, the long-standing rule remains unchanged: cash payments exceeding $10,000 may trigger Form 8300 reporting by dealers.

Why Understanding These Rules Matters for Investors

Interest in physical bullion tends to rise during periods of economic uncertainty. When inflation expectations increase, currencies fluctuate, or geopolitical tensions escalate, investors often turn to precious metals as a store of value.

As gold and silver prices respond to global economic forces, misinformation about government regulation can spread rapidly.

Understanding the actual reporting rules helps investors distinguish fact from rumor and make more informed decisions when buying or selling bullion.

The Bottom Line for Precious Metals Investors

Despite widespread speculation online, IRS reporting rules for precious metals investors have not undergone major changes in 2026. The regulatory framework governing bullion transactions remains largely the same as it has been for decades.

In practice, most reporting requirements apply to dealers and are triggered only under specific circumstances—such as cash payments exceeding $10,000 that require Form 8300 or large wholesale-style bullion sales that may trigger Form 1099-B reporting.

For most individual investors, routine purchases and sales of coins or small bullion bars do not meet these thresholds.

In simple terms, investors should remember:

-

Cash payments over $10,000 may require dealers to file Form 8300

-

Certain large bullion sales may trigger Form 1099-B

-

Profits from selling precious metals may be subject to capital gains tax

As the gold spot price, silver spot price, and broader precious metals markets continue to respond to global economic forces, having accurate information about reporting rules helps investors separate fact from rumor—and focus on building a resilient, diversified portfolio.

Disclaimer:

The information provided in this article is for educational and informational purposes only and should not be considered tax, legal, or financial advice. Precious metals reporting requirements and tax regulations may change, and individual circumstances can vary. Investors should consult with a qualified tax professional, accountant, or financial advisor regarding their specific situation before making decisions related to precious metals purchases, sales, or reporting obligations. Bullion Exchanges does not provide tax or legal advice.

Leave a comment

Gold Bars: 100 troy oz. or 1 kilo (.995 fineness); reportable at one 100 oz. bar or 3 kilo bars

Silver Bars: 1,000 oz. (.999 fineness); reportable at 5 bars (5,000 troy oz.)

Platinum Bars: 10 troy oz. or larger (.9995 fineness); reportable at 50 troy oz.

Palladium Bars: 10 troy oz. or larger (.9995 fineness); reportable at 100 troy oz.

These thresholds determine when a transaction must be reported by a dealer to applicable authorities.